Why Smart Real Estate Developers Are Turning to Gold

By Ladan Hosseinzadeh Sadeghi, President & CEO, Sky Property Group Inc.

TORONTO, ON / ACCESS Newswire / February 24, 2026 / I have spent more than three decades building things. Land. Buildings. Partnerships. Capital positions. And through all of it, I have developed a deep appreciation for one thing above almost all else: assets that hold their value when everything else is uncertain.

That appreciation has led me, like a growing number of serious developers I know, toward a perspective that might surprise people: gold and precious metals deserve a place in every sophisticated real estate developer's portfolio strategy.

This isn't contrarianism. It's arithmetic.

---

The Inflation Problem No One Is Finished Solving

The inflation of the past several years caught a lot of developers off guard, including some very experienced ones. Construction costs spiraled. Labour prices jumped. Material inputs - lumber, steel, concrete - became volatile in ways that upended pro formas that had looked airtight twelve months earlier.

Here's what that period demonstrated: inflation is a real estate developer's most persistent enemy, and traditional financial instruments - bonds, cash positions, even equities - do not reliably hedge against it. When the purchasing power of a dollar is eroding and your costs are denominated in dollars, you need stores of value that move differently.

Gold has been that store of value, reliably, across centuries and across radically different economic regimes. When central banks expand money supply, gold tends to rise. When inflation outpaces official targets, gold tends to rise. When geopolitical uncertainty spikes, gold tends to rise. For a developer navigating a multi-year project cycle, that counter-cyclical movement is not just philosophically appealing - it is strategically useful.

---

What Tariffs and Trade Disruption Are Teaching Us About Supply Chains

The conversation around tariffs has sharpened considerably in recent months, particularly for Canadian developers working in an economy deeply integrated with - and increasingly in tension with - the United States. The implications for construction materials are direct and significant. When cross-border supply chains are disrupted, when steel and aluminum face new duties, when the cost of imported components climbs unpredictably, a developer's input costs can move sharply and quickly.

This is precisely the environment where hard assets earn their keep.

Precious metals - gold, silver, platinum - are not subject to tariff regimes in the same way manufactured goods are. They trade on global commodity exchanges with pricing that reflects global supply and demand. They can be held in physical form or through well-structured financial instruments. They are liquid. And critically, they tend to perform well in exactly the kind of macro environment that puts pressure on real estate development margins: rising inflation, trade disruption, currency weakness, and elevated geopolitical risk.

---

The Relationship Between Real Estate and Commodity Cycles

Something I have observed over my decades in this industry is that real estate and commodity markets are not as independent as they might appear. They are both tied to the real economy in ways that create meaningful correlations at certain points in the cycle and meaningful divergences at others.

In a rising rate environment - the kind we have been navigating - real estate development faces headwinds from financing costs while commodity prices, particularly gold, often hold firm or appreciate. In a period of currency weakness, real property in major urban centres tends to retain value in nominal terms, but so does gold, which is priced in U.S. dollars globally and benefits directly when the greenback weakens.

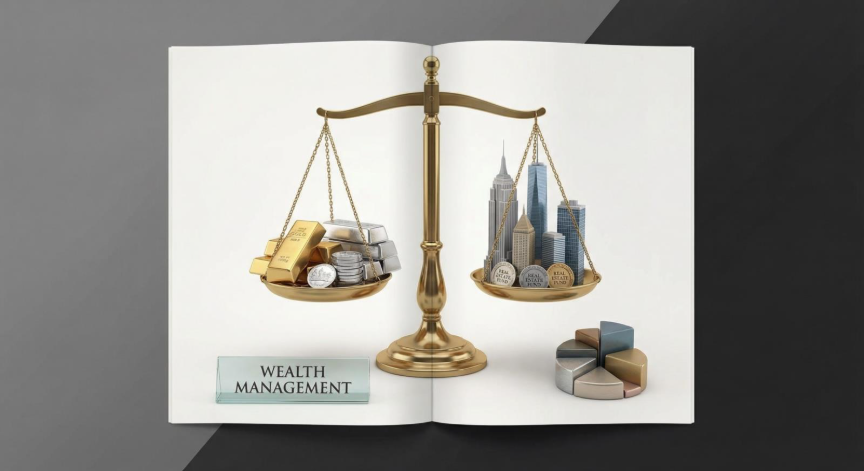

What this means in practice is that a portfolio that includes both real estate and precious metals is not simply diversified in a superficial sense - it is diversified across two asset classes that respond to the same macro pressures differently and often beneficially. They are not perfectly inversely correlated, but the relationship is complementary in a way that reduces overall volatility in a developer's balance sheet.

---

A Practical Framework for Developer Diversification

I want to be clear about what I am advocating and what I am not. I am not suggesting that real estate developers abandon their primary business and speculate on commodity markets. That would be as misguided as a gold investor levering up into development projects without the operational expertise to execute them.

What I am suggesting is more measured: intelligent capital allocation that treats precious metals as a portfolio stabilizer rather than a core business. For a developer with significant illiquid positions - land under assembly, projects in entitlement, pre-construction equity - maintaining a meaningful allocation to liquid hard assets like gold is simply prudent treasury management.

The practical tools to do this have never been more accessible. Physical gold held in allocated accounts, gold ETFs for liquid exposure, silver and platinum for investors willing to accept more volatility in exchange for potentially higher returns, and gold-backed instruments for those who want currency-like liquidity with commodity-like characteristics - these are all well-established instruments with deep markets.

The key discipline is treating this allocation as a hedge, not a trade. Set a target allocation - often discussed as five to fifteen percent of a developer's liquid reserves, though circumstances vary enormously - and maintain it through rebalancing rather than trying to time gold's movements against real estate cycles.

---

Why Now Matters

The confluence of factors we are navigating in 2026 makes this conversation particularly timely. Construction cost inflation remains elevated. Trade policy uncertainty is creating material supply chain risk. Currency markets are volatile. Central banks globally have been net buyers of gold for several consecutive years - a signal worth paying attention to.

The developers I respect most in this industry are not the ones who succeeded in one market cycle. They are the ones who built organizations and balance sheets that survived multiple cycles, including the difficult ones. They did it by being excellent at their core business and disciplined about protecting capital from the risks they could not fully control.

Gold and precious metals are one tool in that toolkit. Not the only one. Not always the most important one. But in the current environment, one that deserves a serious look - and a real allocation.

---

The views expressed in this article are those of the author and do not constitute financial or investment advice. Individuals should consult their financial advisors before making investment decisions.

Contact Information

Ladan Hosseinzadeh Sadeghi

[email protected]

SOURCE: Sky Property Group Inc.

View the original press release on ACCESS Newswire

P.Navarro--TFWP